Samsung Electronics Labor Dispute: Valuation Impact Analysis Under Profit-Sharing Scenarios

May 15, 2026

Current Issue in Valuation

Samsung Electronics has reported record earnings as demand for AI-related memory semiconductors accelerated sharply. The semiconductor division has emerged as one of the largest beneficiaries of the global investment cycle surrounding AI infrastructure, hyperscale data centers, and advanced AI servers.

At the same time, labor negotiations have intensified. The union has argued that employees should receive a larger share of the semiconductor division’s extraordinary profits through expanded performance-based bonuses. Management, meanwhile, has attempted to preserve the existing compensation framework while proposing a more flexible special incentive structure.

Because Samsung Electronics is currently operating during a period of unusually strong profitability, even relatively small changes in compensation policy could produce meaningful changes in earnings, margins, and ultimately equity valuation.

For students studying Financial Statement Analysis and Valuation, this issue presents an especially interesting case. It demonstrates how labor policy, compensation structure, and stakeholder negotiations can directly influence corporate valuation during a period of extraordinary earnings expansion. For that reason, this article provides a simplified valuation analysis of the potential impact of profit-sharing scenarios on Samsung Electronics’ equity value.

Current Valuation Estimate

This analysis focuses on estimating Samsung Electronics’ current valuation and examining how different profit-sharing structures may affect shareholder value. In particular, the analysis evaluates multiple what-if scenarios based on varying profit-sharing ratios and their potential impact on short-term growth expectations.

The primary objective is to understand how labor compensation policy may influence valuation during an exceptional earnings cycle driven by the rapid expansion of AI-related semiconductor demand.

The first step of the analysis is estimating Samsung Electronics’ current valuation under base-case assumptions. The model assumes FY2026 operating profit of approximately KRW 343.85 trillion, reflecting continued strength in AI semiconductor demand and sustained pricing momentum in the memory market.

This represents an extraordinary increase from KRW 43.6 trillion in 2025, highlighting the scale of the current AI-driven earnings expansion.

Under this framework, the baseline valuation reflects prevailing market expectations before incorporating any additional labor-related expenses or operational uncertainty arising from the ongoing labor dispute.

Valuation What-If Analysis

The core of this article is the valuation sensitivity analysis, which examines how Samsung Electronics’ estimated equity value shifts under varying combinations of profit-sharing ratios and short-term growth assumptions.

The analysis specifically evaluates how the company's equity value fluctuates as profit-sharing scenarios range from 5 percent to 30 percent, while short-term growth assumptions are adjusted from positive 10 percent to negative 4 percent.

While the base-case assumption for short-term growth is 10 percent based on the current surge in AI-related semiconductor demand, higher profit-sharing ratios may negatively affect this trajectory through the prism of the Opportunity Cost of Capital. In a highly capital-intensive industry like semiconductors, cash diverted to labor compensation represents a direct reduction in the liquidity available for R&D and CAPEX (Capital Expenditure). As these resources are shifted from productive asset reinvestment to immediate labor costs, the firm faces a heightened risk of eroding its future competitive advantage in the next-generation AI chip race. Consequently, aggressive profit-sharing does not merely increase operating expenses; it potentially weakens the firm’s long-term growth trajectory by delaying critical investments in technological leadership.

For this reason, the analysis assumes a gradual deterioration in short-term growth expectations as profit-sharing levels increase. Accordingly, the growth assumptions decline sequentially across the sensitivity framework to capture the market’s concern that immediate payouts might come at the expense of future market dominance. The framework is ultimately designed to evaluate the interaction between two major forces: direct earnings dilution resulting from higher labor compensation and the potential deterioration in investor expectations regarding future growth momentum during the AI semiconductor cycle. As a result, the analysis captures both operational pressure and market sentiment pressure simultaneously.

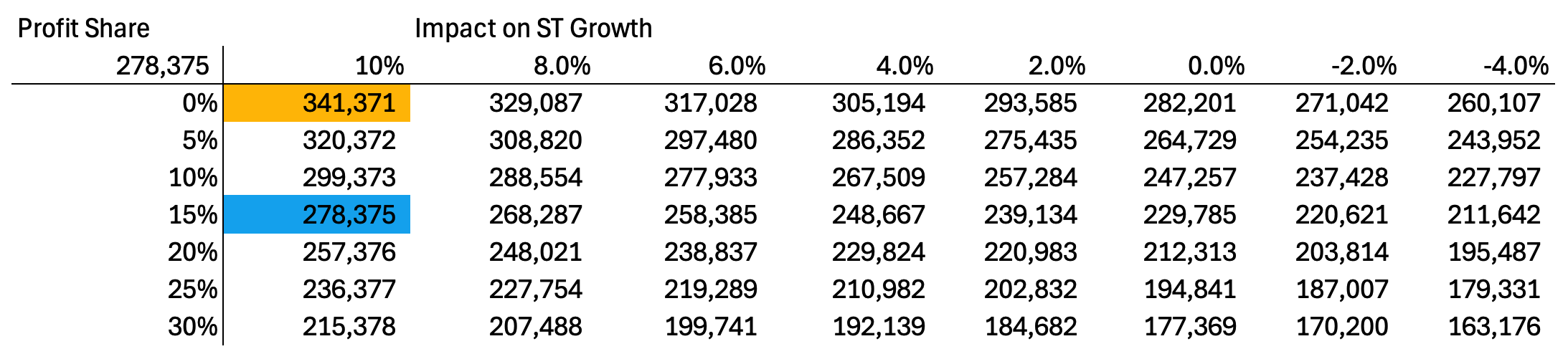

Main Sensitivity Table

The following table represents the central result of the analysis. It illustrates how Samsung Electronics’ estimated valuation changes under different assumptions regarding labor compensation and short-term growth expectations. These values were calculated using the Residual Income Model (RIM), which accounts for the cost of equity to determine the firm's intrinsic value based on future earnings potential. The detailed financial assumptions, modeling process, and underlying valuation methodology are not discussed extensively in this article.

Data source: DataGuide

Using simplified assumptions, the intrinsic value of Samsung Electronics is estimated at KRW 342,371 per share under the base-case scenario. If the company shares 15 percent of operating income with employees while maintaining short-term growth at 10 percent, the estimated intrinsic value declines to KRW 278,375 per share.

The sensitivity analysis demonstrates that valuation becomes increasingly vulnerable as profit-sharing ratios rise and growth expectations weaken. During periods of strong AI-driven expansion, investors may tolerate higher labor costs because earnings growth remains sufficiently strong to offset margin pressure. However, when growth expectations begin to moderate, the negative effect of compensation expansion becomes significantly more severe.

This dynamic is particularly important in the semiconductor industry, where valuations are highly cyclical and small changes in profitability or growth assumptions can produce disproportionately large changes in equity value.

The analysis also suggests that labor-related uncertainty may affect valuation beyond the direct accounting impact of compensation expense. If investors begin to perceive labor disputes as a longer-term operational risk, valuation multiples themselves may contract in addition to earnings reductions.

Conclusion

Samsung Electronics’ labor dispute represents more than a conventional wage negotiation. It is increasingly becoming a broader test case for how AI-era semiconductor profits are distributed between labor and shareholders.

The sensitivity analysis demonstrates that profit-sharing policy can materially affect valuation, while the resulting impact on short-term growth expectations can amplify downside pressure further. In other words, the market impact of labor negotiations may ultimately exceed the immediate financial cost of profit sharing itself.

As AI-driven semiconductor demand continues to reshape the semiconductor industry, investors must evaluate not only technology leadership and earnings growth, but also labor structure, compensation philosophy, and operational resilience.

Under aggressive profit-sharing scenarios combined with weaker short-term growth expectations, the valuation implications could become substantial.